This is the second in a series of essays on the 6 Foundational Principles of Holistic Financial Wellness that I describe in my new book “Money Mountaineering.” In this one, I want to talk about “Debt” in a more general sense. As we look at our personal financial balance sheets we have many obligations that might be satisfied by money, but many of those obligations were incurred through the receipt of goods, and services that are often not measurable in dollars and that the terms of repayment are far from clear. How to view these debts and how they affect one’s financial well-being is a very tricky issue and whole books could be written on the subject.

My goal here is to simply bring your attention to those liabilities and to both caution you against ignoring them, as default can lead to real financial problems, while at the same time recognizing that many of these liabilities can be satisfied using other assets at your disposal thereby contributing in a meaningful way to your overall financial well being.

Keeping the lights on with home-cooked meals.

My neighborhood in the old West End of Santa Rosa is filled with old houses in serious need of repair. Many of my neighbors rent these houses from landlords who take a “just in time” approach to the maintenance of their properties or in some cases live in houses that are owned by family members who live in different towns.

Many of these neighbors come to me for financial advice and among the more difficult questions that they ask me is what to do when the material things in their lives break and need to be fixed so that they continue to work and have the basics we all need to survive (shelter, light, heat and running water).

It turns out that my actuarial training and facility in financial analysis are of limited use in solving their problems. Instead, an expanded view of what they need and what they have to offer others is required.

My friend Linda lives down the block from me in a house that is well over 100 years old. While the foundation, plumbing, and electrical systems are not quite that old, the house is in sore need of renovation.

The house is owned by another family member – Grandpa Joe who lives 60 miles away and is, himself, getting on in years, relying on the already reduced rent that Linda pays him to supplement his small pension and Social Security.

It’s not that Joe and Linda don’t have material assets that theoretically could be used to make the house safe and livable again. After all Joe owns the house and has only a minimal mortgage outstanding while Linda has accumulated 50 years’ worth of antiques and collectibles that these days have a considerable monetary value. The problem is that converting those “real” assets into dollars is easier said than done, and when I looked at their situation, the numbers simply didn’t work.

However, both Joe and Linda have many other assets that can be brought to bear on the problem. In particular, they each have many relationships that are extremely valuable. Specifically, Joe has many close friends who are skilled tradesmen (plumbers, electricians, carpenters, etc.) who are always looking for “side jobs”, and while Joe does not have skills that can be used here (he is a locksmith by trade), with these contacts, he was able to very quickly arrange for the house to be fixed. Many of these tradesmen have had their businesses helped by Joe and as a result, are only too happy to pay off their “debts of gratitude” by coming by and assessing what work is needed to be done.

For her part, Linda is a spectacular cook and her holiday dinners are legendary among those who have been lucky enough to have attended one. And good food is only part of the reason that an invitation to Linda’s house is so sought after. The history, art, and relics that fill Linda’s house are just as nourishing and tasty as the food she serves. Neither Joe nor Linda have the financial wherewithal to pay the cost of what typical home repair companies charge, but between the lunches, dinners, and stories that the two of them provide, the crews that come to work on the house always feel well compensated for the services they provide.

And so, having had to admit that some problems can’t be solved with actuarial analysis, I watched with fascination as a succession of vans and trucks came and went to Linda’s house while small crews of electricians, plumbers, and carpenters rewired the house, upgraded the kitchen and replaced doors and drywall throughout the house, while the din of power tools, late 60’s music, and happy voices emanated from the little green house down the block beginning early in the morning and lasting until well past sunset.

It’s one thing to look at a Gift Economy from a distance and consider it as a system that may or may not be a viable alternative to one based on free-market principles. It’s quite another to watch it in action. Many believe in the Gift Economy and are trying to design and implement one for communities and organizations. I applaud that effort and hope that such efforts succeed, but I also think that change like this happens from the ground up, and just needs to be recognized and encouraged to grow whenever it naturally arises.

The truth is that all of us already participate in a Gift Economy in our own lives, even if it only encompasses what we do for our own families and close circle of friends. We all give to those we care about and we all owe debts of gratitude to those who have given to us.

So how do we account for these “assets” and “liabilities” on the karmic balance sheet of life? I would suggest that we don’t even try to measure them, but instead that we simply recognize when such obligations exist and understand that evening the scales will take time, energy, and even sometimes “real” money, and that “investing” in giving to others will often yield a return that is far greater than any financial analysis will reveal. In my opinion, the sooner we recognize that such non-monetary exchanges of value are taking place and consider the gifts we give and receive as part of our overall financial situation, the closer we will come to achieving true holistic financial wellness.

About Peter Neuwirth: Since graduating from Harvard with a degree in mathematics and linguistics in 1979, Peter Neuwirth has held actuary leadership positions at consulting firms including Aon, Hewitt Associates, Watson Wyatt Towers, Perrin, and Towers Watson. He also ran the actuarial firm Coates Kenney and spent a year at Price Waterhouse.

Currently a Fellow of the Society of Actuaries and the Conference of Consulting Actuaries, Pete regularly consults with the largest corporations in the world about their retirement plans with a focus on time risk and money. “These fundamental concepts shape our world,” explains Pete, who is a sought-after speaker for professional conferences, and is frequently quoted in national mainstream and trade publications.

After being asked too many times “What is an actuary, exactly?” Pete has written two books to answer another question: “How does an actuary think, and why does it matter?”

His first book, What’s Your Future Worth, is an accessible step-by-step guide to using the powerful concept of Present Value. Pete explains, “My goal is to help readers determine the value today of something that might happen in the future and evaluate outcomes that might arise from choosing one path instead of another.”

In his newest book, Money Mountaineering, Pete shares his views on the challenges we face to survive and thrive in a complex uncertain noisy and sometimes irrational wilderness. “I hope to help readers better understand the financial world they must live in and what they must do to make their way through it,” Pete shares.

Pete is also a senior consulting actuary for CapAcuity a member of the University of Illinois Academy for Home Equity in Financial Planning and the outside director at Rael & Letson. He is a longtime resident of Sana Rosa, CA. Learn more at www.peterneuwirth.com.

“Everything changes a little as it should. Good ain’t forever, and bad ain’t for good,” — Roger Miller from “Lou’s got the Flu”

I learned a lot from my mathematician father and as many lectures as he gave me growing up, there was almost always music playing in our house. Roger Miller’s songs formed the soundtrack to many of my childhood Sunday afternoons.

I always listened to the words of the songs and from the men and women who sang them I learned even more. As rigid and clear as my father’s views and teachings usually were, he was always open and curious about the world around us and how it can change – in unpredictable ways that can render one’s normal survival strategies a recipe for suffering.

As a precocious child in the 1930s and 1940s, my dad watched as the world run by the grown-ups got turned inside out and upside down for reasons that people still argue over. Geography must have been a particular challenge for his elementary school teachers. World maps, only recently revised to reflect the geopolitical shifts caused by World War I, became a moving target. Whole fields of study had to be modified on the fly to keep up with events, while only the oldest and most solid academic subjects remained the same. And this not even considering the socio-economic and geopolitical changes that were occurring in real-time disrupting normal life outside of school.

The list of academic subjects unaffected by World War II was relatively short. Astronomy and science where new discoveries come more slowly could be considered one. Ancient history and Classic literature were perhaps two others with a long lead time between the writing and the recognition of a work’s value, but the most unchanging of all fields was and always has been mathematics. That is a very good thing since it is through mathematics and mathematical thinking that we can understand the changes themselves.

We are not in a time of war in the U.S., but whatever changes this country is going through now, they seem as dramatic to me as any I have seen in my 64 years on earth, and I feel grateful to my father for having passed on to me the wherewithal to use a mathematical lens to consider what is happening around us.

I am an actuary and not a mathematician and so, haven’t used the gifts he gave me in the same way as he did. Rather than attempt to climb the highest peaks of mathematical abstraction as he and his colleagues have, I chose to concern myself with the more mundane world of Money. It is an area where I can use the skills he taught me to separate the signal from the noise, and it is an area where I think some of my insights can help others.

In Money Mountaineering I lay out 6 Foundational Principles of Holistic Financial Wellness.

Holistic Financial Wellness Principle #1: Every person’s values, objectives, and financial situation are unique and multi-dimensional. Therefore, make every financial decision consistent with who you are, considering the totality of your own specific financial picture.

Putting aside whether “who you are” is changing as the world changes around you, to apply this principle effectively, it is critical to understand and be clear on your “values, objectives and financial situation”. Reading Money Mountaineering won’t help you determine whether and how your values have changed – but the tools I provide might help you better understand how your financial situation and its relationship to the financial world, in general, has changed, and by understanding that, you can, if warranted, take a fresh look at your objectives – where you want to hike, climb or camp in the financial wilderness.

In Money Mountaineering I described in some detail my own financial situation and the complicated set of investments and income-generating ventures I was involved with, but things change – and sometimes, as Roger Miller says, “everything changes”. In my case, it was almost everything and the changes were far from “little”.

For me, losing my home and everything in it in a wildfire that raced through my part of the world 9 months ago was just the beginning. Now, instead of living on 8.5 acres in the relative solitude of backcountry Sonoma County, I live near downtown Santa Rosa in a rented house that I have filled with a mix of new rental furniture (provided by my insurance company) and well made, used furniture that I purchased from local merchants or received as gifts from friends and neighbors. I have also begun to replace all the books and technology (phones, appliances, etc.) in my life so I can be more engaged with the larger world around me.

That process has been both transformative and educational as I have developed connections with dozens of local merchants and neighbors who are now an essential part of my new situation. I am the same person I was before the fire, but my network of friends is different as well as the community that I am a part of. And those changes have had a large impact on not just my financial objectives but what my hopes, dreams, and fears are about the future.

On top of that, I see the economic and financial markets undergoing dramatic change as well. These kinds of changes are much more familiar to me as I have been watching markets evolve and change continuously for over 40 years. Not that the environment is exactly like anything I have seen before, but the forces at work are, at least to my eyes, the same as they’ve been for decades.

So what does that mean for the financial steps I plan to take in the near future? Well, the first thing I am doing is placing a higher value on real assets than I have in the past. Much of the furniture I purchased (or was given to me) is old and not only useful but in many cases is better made and more durable than what I can get new. Not only that, but with inflation apparently increasing (perhaps as a result of the Fed’s heroic efforts to avert a financial collapse by flooding the economy with trillions of dollars) I believe that my new acquisitions are likely to increase in value rather than depreciate as most new things often do. In terms of my invested assets, I am therefore shifting some financial assets into collectibles that I like having around like comic books, coins, and old books.

More generally, I am now recognizing that the relationships I have with my community in Santa Rosa are among the most precious components of my life that exist. I am learning how to nurture and grow those relationships and one of the best ways I have discovered for doing that is through giving and receiving gifts. In Chapter 15 of my book, I make a case for the “gift economy” and now for the first time in my life, I am getting an opportunity to participate in one that is growing here in my new neighborhood in a way that may bear some surface similarities to the parking lot of a Grateful Dead concert (the gift economy I am most familiar with) but is on a larger scale and potentially more sustainable and permanent than a caravan of buses following a band from town to town. Whether a gift economy can take root and grow in something as large as a city or a county is a question that I don’t know the answer to, but right now I am simply adjusting my financial plan to the realities in my environment and the new financial situation I find myself in.

I hope this essay will give my readers a fuller understanding of HFW Principle #1. In particular, it is important to know that using this principle is not a “set it and forget about it” proposition, but rather a step that once undertaken must be reviewed periodically as you and the world around you change. In future essays, we will take a deeper look at the other 5 principles, but consider this as me sharing my first step back towards holistic financial wellness. I am glad to have you along for the journey.

About Peter Neuwirth: Since graduating from Harvard with a degree in mathematics and linguistics in 1979, Peter Neuwirth has held actuary leadership positions at consulting firms including Aon, Hewitt Associates, Watson Wyatt Towers, Perrin, and Towers Watson. He also ran the actuarial firm Coates Kenney and spent a year at Price Waterhouse.

Currently a Fellow of the Society of Actuaries and the Conference of Consulting Actuaries, Pete regularly consults with the largest corporations in the world about their retirement plans with a focus on time risk and money. “These fundamental concepts shape our world,” explains Pete, who is a sought-after speaker for professional conferences, and is frequently quoted in national mainstream and trade publications.

After being asked too many times “What is an actuary, exactly?” Pete has written two books to answer another question: “How does an actuary think, and why does it matter?”

His first book, What’s Your Future Worth, is an accessible step-by-step guide to using the powerful concept of Present Value. Pete explains, “My goal is to help readers determine the value today of something that might happen in the future and evaluate outcomes that might arise from choosing one path instead of another.”

In his newest book, Money Mountaineering, Pete shares his views on the challenges we face to survive and thrive in a complex uncertain noisy and sometimes irrational wilderness. “I hope to help readers better understand the financial world they must live in and what they must do to make their way through it,” Pete shares.

Pete is also a senior consulting actuary for CapAcuity a member of the University of Illinois Academy for Home Equity in Financial Planning and the outside director at Rael & Letson. He is a longtime resident of Sana Rosa, CA. Learn more at www.peterneuwirth.com.

Barry Sacks Ph.D. earned his Ph.D. in semiconductor physics from M.I.T., then taught at U.C. Berkeley. He earned a J.D. from Harvard Law School and is a Certified Specialist in Taxation Law from the California Board of Legal Specialization.

After spending 35 years as an ERISA attorney specializing in qualified retirement plans, he used his breadth of skills to discover a role for a reverse mortgage to help make a retirement portfolio last longer. Barry now has a law practice providing special services to tax professionals in the area of “Offers in Compromise” for retirees living on 401(k) accounts or securities portfolios.

With his brother, Professor Stephen Sacks, Barry published the pioneering research paper modeling a strategy that uses reverse mortgage credit lines to mitigate the effects of adverse sequences of investment returns in retirement accounts (Journal of Financial Planning, February 2012). A sequel to this paper expanding the range of applications of the strategy was co-authored by Peter Neuwirth, FSA, and Stephen Sacks. Read all about it.

While developing his model for reverse mortgages in retirement income planning, Barry became aware of the particular needs of retirees and soon-to-be retirees in the process of divorce. These needs are of special concern in cases where the retirement savings are divided between the parties or where one of the parties has received most of the retirement savings but not much of the value of the home equity. Learn more here.

“We weigh every significant decision based on how it will affect our future,” explains actuary Peter Neuwirth, author of What’s Your Future Worth? “But when it comes to figuring that out, we mostly make the process up as we go along.”

While he can’t help you actually predict the future, Pete can offer a simple, systematic way to make much better guesses about it—and so make better decisions.

In What’s Your Future Worth:Neuwirth offers an accessible, step-by-step guide to using the powerful concept of Present Value—which allows you to determine the value today of something that might happen in the future—to evaluate all of the outcomes that might arise from choosing one path as opposed to another. Using examples that anyone can relate to, Neuwirth walks you through the process. Your old refrigerator doesn’t work as well as it used to—should you buy a new one right away or muddle through for a while? You’re offered a great discount on a service you don’t need at the moment but eventually will—buy the service now or wait?

With just a little math and some common sense: Compare future costs and benefits with present costs and benefits and make “apples to apples” comparisons. This book will be indispensable for anyone who has ever had to figure out whether to stick with an awful job or follow his or her bliss, fix that old car or buy a new one, increase 401(k) contributions or keep the same take-home pay, and a thousand other decisions.

This week on Margaritas with Marguerita: Our guest Peter Neuwirth, author of "Money Mountaineering," explores the world of money and provides his views on its nature and the challenges we all face as we try to survive, even thrive, in this complex, uncertain, noisy, and sometimes irrational wilderness. Learn all about it!

A Note from Marguerita Cheng, CFP® Pro — I invite you to tune in for this week’s episode of my podcast and video show, Margaritas with Marguerita, where for 15 minutes each Friday at 5 pm EST, women learn from industry experts how to flex their financial muscles live on Facebook.

Meet our guest: Peter Neuwirth, author, Money Mountaineering: Using the Principles of Holistic Financial Wellness to Thrive in a Complex World and What’s Your Future Worth: Using Present Value to Make Better Decisions

Today’s topic: Money Mountaineering — The 6 foundational principles of Holistic Financial Wellness, including practical things people can do to achieve and maintain financial wellness.

Rita asks Peter:

Money Mountaineering lays out 6 principles to achieve and maintain financial wellness. Can you tell us what they are and why they are important?

Your principle #3 says that individuals should get financial advice from experts who are “100% on your side”. Is that possible these days, and how do you do it?

Your book was named as one of the 12 best business books of 2021for advisors. Which of the other 5 principles you describe would you say are the most important for Financial Planners to keep in mind as they develop financial strategies for their clients?

I understand you have a new webinar in development around how to plan for retirement in today’s complex and uncertain world. can you tell me a little bit about it?

You talk about 3 tools to put in your backpack. How do those 3 relate to the “3 legged stool” that many of us used to use in talking to our clients about retirement income strategies?

About Peter: Peter Neuwirth has been an actuary for more than 40 years and after decades of having been asked too many times, “What is an actuary exactly?” he has decided to go beyond answering that question to answer another: “How does an actuary think and why does it matter?”

Peter’s work is well known in actuarial circles. He is a frequent speaker at professional conferences and has been quoted in both the mainstream and industry press on actuarial matters. He is a Fellow of the Society of Actuaries and a Fellow of the Conference of Consulting Actuaries.

Peter has consulted with dozens of the largest corporations in the world around the Retirement Plans they sponsor and pay for. This experience has provided him with a deep practical understanding of three of the fundamental concepts (time, risk, money) that shape our world. Many of those insights are shared in Peter’s books and essays.

Peter’s first book, “What’s Your Future Worth” provides an accessible, step-by-step guide to using the powerful concept of Present Value—which allows readers to determine the value today of something that might happen in the future—to evaluate all of the outcomes that might arise from choosing one path as opposed to another.

In this “Money Mountaineering,” Peter explores the world of money and provides his views on its nature and the challenges we all face as we try to survive, even thrive, in this complex, uncertain, noisy, and sometimes irrational wilderness. This is a book designed to help readers understand what kind of advice they truly need—to gain a better understanding of the financial world they must live in and what they must do to make their way through it.

With a reputation among his peers as being a creative, knowledgeable, and experienced actuary with a penchant for both problem solving and thinking “outside of the box” Peter is also a storyteller who believes that story of the actuarial perspective is one that needs to be told.

Pete lives in Santa Rosa, California. You can visit his website and read his essays at peterneuwirth.com.

Ongoing Research Project at University of California at Santa Barbara

By Janet Duncan FCAS, FSA, Ian Duncan FSA, Pete Neuwirth FSA, FCA, and Barry Sacks JD, Ph.D

HUD/FHA Guarantees and the MMI Fund

HUD/FHA guarantees are critical to the long-term viability of the HECM market as well as the effectiveness of retirement income strategies employed by “house rich” retirees utilizing HECM’s

FHA guarantees are funded via up front and ongoing “Mortgage Insurance Premiums” (MIP’s) set by HUD

MIP’s historically set at 0.5% (of home value) up front and 1.25% (of outstanding loan balance) ongoing, but effective 10/2/17, MIP rates changed to 2.0% up front and 0.5% ongoing

MIP’s held in MMI Fund whose solvency has recently become a concern

2016 valuation (performed by IFE) showed a long term $7.8 billion deficit, while 2017 valuation, (performed by Pinnacle Associates) showed a deficit of $14.2 billion

The Pinnacle Valuation of MMI Fund solvency

Major focus of Pinnacle analysis was on evaluating short-term risks and funding shortfall associated with current portfolio

Closed group valuation focuses on status of existing

HECM’s and incorporates pre 2017 MIP structure

Includes detailed review of home price volatility, borrower “default” experience (e.g. via failure to pay property tax) and the transaction costs associated with a forced sale

Current borrower profile and behavioral assumptions (e.g. HECM drawdown timing and likelihood of property tax/insurance default) seem inconsistent with likely market/demographic trends

Outline of Current Research Project

Built new model to test adequacy of the current MIP structure to fund the promised HUD/FHA guarantees and potentially eliminate existing MMI Fund deficit

Utilizes long term (retirement) actuarial principles and is designed to perform an Open Group valuation

Can highlight impact of new MIP rates, possible changes in borrower profile and broader use of alternative LOC drawdown strategies (e.g. the “coordinated strategy”)

Basic model has been constructed and tested on publicly available data on HECM’s initiated 1989-2011

Preliminary findings indicate reasons to be optimistic about the future solvency of the MMI Fund

Preliminary Findings

Analysis of 158,000 HECM’s that terminated between 2005 and 2011 indicate that such terminations would have produced a net gain for MMI Fund had new MIP rates been in effect when HECM’s initiated

Significant differences in potential claims found by size of HECM (higher HECM values produced lower claims)

Potentially longer duration of HECM and lower property tax/insurance default rates (if borrower profile changes as expected) suggest future HECM’s will produce a surplus for the MMI Fund

If future HECM’s produce surplus and HECM volume grows significantly then projected deficit of MMI Fund will potentially disappear

This very personal book about finance ends with a description of the author’s Sonoma County, Calif., residence being burned to the ground in 2020 by the fearsome Glass Fire. Peter Neuwirth had 15 minutes to evacuate. What to take? In every room, there were objects of different value, utility and sentiment. Into a suitcase went his passport, will, some family photos, laptops, notebooks. Also, some baseball cards and Grateful Dead concert ticket stubs. Even actuaries can’t account for sentiment. Finally, he grabbed two books. The titles are a clue to the author’s intellectual heritage.

In Money Mountaineering, Neuwirth, trained as an actuary, reveals his investing philosophy. He shares in considerable detail how he has organized his finances. Rarely has a business author been so self-disclosing. Readers get a tightly argued discourse on investing, debt, uncertainty and the future of money. Most fun is his takedown of popular financial gurus such as Suze Orman and Dave Ramsey, whose collective advice Neuwirth demolishes as mistaken and dismisses with relish.

Key Chapter

Chapter 5—“Charlatans, Fools, and Snake Oil Salesmen”

Key Quotes

“Every person’s values, objectives, and financial situation is unique and multi-dimensional.”

“Debt is neither good nor bad but is always important—as important as your money or any other asset that you may own.”

“It is important to take full ownership of your own financial situation. Know what you can’t do yourself, and make sure those you hire are 100 percent on your side.”

“Learn to live with uncertainty and have a financial strategy that has flexibility and optionality built into it.”

“Organizing your financial life to survive a severe economic or life event is essential for long-term financial health.”

“Financial health comes from fearless self-awareness and acknowledgment of our cognitive and emotional limitations as human beings.”

Welcome to my second book where I explore the world of money and provide my views on its nature and the challenges, we all face as we try to survive, even thrive, in this complex, uncertain, noisy and sometimes irrational wilderness, explains actuary Peter Neuwirth.

So, is this another financial advice book? Not exactly, rather this is a book designed to help you understand what kind of advice you truly need. My goal is to help you gain a better understanding of the financial world you must live in and what you must do to make your way through it.

In particular, I want to help you determine:

What you can decide for yourself- almost certainly more than you’ve been led to believe.

Where you need help- probably in different areas than you think.

What trustworthy sources are out there- fewer than you might hope.

This book is not for those who are “too rich to care.” Nor will you get much value from this book if you have no financial resources at all and worry about simply getting by from one day to the next. This book is for the vast numbers of people who are in the middle; those who struggle with the trade-offs between saving for retirement and saving for a down payment on a house. It is for those who can’t decide whether to pay off a student loan early or “double down” and borrow more to start a business. It is for those about to retire who need to figure out when to take Social Security, how much to withdraw from their 401(k) accounts, and whether to downsize their home or take out a reverse mortgage to supplement their retirement income. It is for anyone who has a complicated financial life in which it’s not only challenging to find answers, but it also isn’t clear what questions to ask.

You won’t find any easy solutions to your financial problems in this book. You may find, however, that this book will give you the ability to ask the right questions, and as a result, begin to make better choices.

Think of the world of money as a dangerous and unknown mountain wilderness full of unseen perils, inhabited by wily predators of all sorts. You have found yourself stranded and lost, and in addition to simply surviving and figuring out where you are, you also want to make your situation as comfortable and stress-free as possible, so you have the time, energy, and resources to make the best of the rest of your life.

Having been around the Insurance Industry for over 40 years, I have learned a few things about the business model that has kept large carriers alive and profitable for decades and sometimes centuries (several of the big ones have been around since the 19th century).

One of the key principles I have seen in operation is that hazards almost never turn out as bad as policyholders fear – except when they turn out much, much worse. As a result, insurance companies are able to charge premiums that will generate a profit but do need to attend to the possibility of a “black swan event” that could be truly catastrophic. Fundamentally much of insurance is based on the fact that even though we live in a “fat tailed” world where the mean is far greater than the median, most consumers, even the most sophisticated ones, operate as if risks follow a Normal distribution. In a sense this creates a win-win situation where policy holders feel they are getting risk protection at a reasonable price, while the carriers, with their huge cash reserves, underwriting protocols and re-insurance treaties to protect them from catastrophe, continue to make a good profit collecting premiums in excess of claims.

When it comes to this pandemic, we can see this principle at play in real time. COVID-19 is a quintessential black swan, and when it came ashore early last year, I along with many other actuaries, tried to figure out just how bad this scourge was and most importantly, how bad was it going to get. My particular focus was on COVID-19 mortality, in part because it seemed to be the one aspect of the pandemic that was more tractable than the others (i.e., people are either alive or dead) and partly because mortality risk is so central to the health of the Life Insurance Industry.

It was tricky because data was hard to come by and the disease itself was poorly understood. Nevertheless, in June of last year, I put together an analysis of COVID mortality and published an article on how many people would ultimately die of the disease. My conclusion was that by the time a vaccine was generally available 475,000 people would have died from COVID. The article is available here.

My conclusion, which I believe has proven correct, was that this disease is terrible, but not quite as terrible as people feared. Most pundits at the time were expecting deaths to be well over a million before the pandemic ended, and while my article was well received, there were many who thought I was being overly optimistic about the future course of the pandemic.

With the pandemic now easing its grip on us and vaccines beginning to be generally available, I thought it was time for a follow up analysis.

An updated analysis of COVID mortality

Late last summer, I had actually begun to look at how my projections were turning out and was somewhat disturbed to find that the CDC data I had relied on was becoming messy and difficult to parse. In particular, beginning with some County health departments in Texas, the definition of what constituted a “COVID-19 death” began to shift from “dying from COVID” to “dying with COVID” (i.e., even if you die from a stress induced heart attack after having contracted the disease you are included in the count).

You can read about how and why the change was made here. I don’t doubt that this change was made with the best of intentions, but unfortunately when you change definitions like this, analysis becomes much more difficult.

The good news is that Life Insurance companies are primarily interested in the fact that a death occurred rather than the specific reason for the individual’s demise. As a result, when I took a fresh look at the data, I focused on the number of “extra deaths” that we have experienced as a result of living (and dying) with the disease. I also talked at length with my colleagues at various life insurance companies to find out how worried they were about any “underwriting apocalypse” that might befall the industry.

It turns out that the CDC continues to keep very good data on total deaths even though the number of “COVID deaths” for reasons noted above is pretty noisy, and in particular very difficult to use to compare the direct impact of the virus in the autumn to that experienced during the early part of the year. To address this challenge, I developed a baseline of “normal deaths” and compared that to what happened in 2020 which differed from prior years due to the presence of the virus in our midst. This effort was complicated because of various factors including population growth and the normal seasonality of mortality (November- March generally being the most lethal months), but in the end, I believe I was able to at least see the big picture of what is going on.

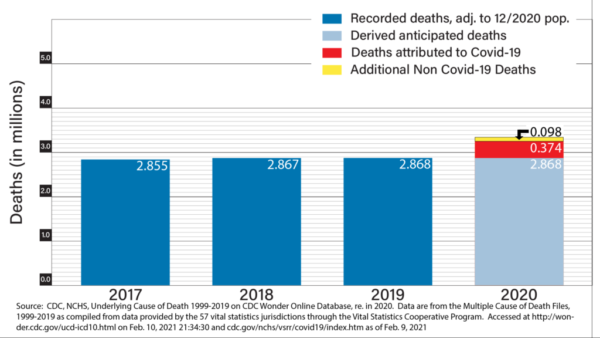

By comparing deaths in 2020 to those in 2017-2019 (adjusting for population changes in the last 4 years), I found that while the number of reported COVID deaths in 2020 was 374,121 (a mix of those dying “from” and those dying “with” the disease) there were 472,116 “excess deaths” relative to what we would actuarially expect during 2020. The difference between these two numbers (97,995) is the number of people who died from the indirect effects of the pandemic. In my June article, I had looked at this and found that in the early days of the pandemic, there were actually less total people dying of non-COVID causes than expected, mostly due to reduced auto accidents and flu deaths. While this was good news, I speculated then that once the effects of deferred medical care and economic hardship began to affect mortality, we could see this trend reverse. It seems that this has happened, and the important question now is whether these secondary effects will persist or fade away when the pandemic ends. The chart below summarizes these numbers and notes where the data comes from.

Needless to say, 374,121 COVID deaths and 472,116 excess deaths are both big numbers, but when we really look at the impact of this increased mortality risk on the Life Insurance industry, we find that the current financial impact is very mild and no one within the industry whose career depends on it seems particularly worried. I am not sure why this is the case, but my guess is that because those that died because of the pandemic had less life insurance than the average American.

That is not to say, that Life Insurance companies are ignoring COVID, but at least within the product lines that I am most familiar with, i.e., Corporate Owned Life Insurance (COLI) and Whole Life Insurance, what I am seeing is modest adjustments in underwriting standards and virtually no changes in the premiums that policyholders are being asked to pay.

I recently spoke with some of the executives at major carriers to get their view of COVID’s impact on their life insurance products. What they told me was that as a general rule, underwriting issues around COVID mortality are far less a concern than the continued low interest rate environment and the potential for corporate income tax rates to increase substantially under the new Democratic administration. It seems that both of these macroeconomic factors pose greater challenges and opportunities for the industry than the prospect of many more COVID deaths. That being said, the industry is responding to all three of those aspects of the current environment.

With respect to the two economic issues, the folks I talked to are quite optimistic about the future of COLI. With higher tax rates, COLI will become a much more tax efficient corporate financing vehicle for numerous purposes, and while chronically low interest rates make “fixed” products perform worse, insurance companies are responding by shifting resources toward their “variable” products where recent stock market performance has made those products particularly attractive.

With respect to COVID specifically, it appears that claims have not materially increased during the pandemic, perhaps due to the sad fact that many of those who have died from the disease had limited or no life insurance. In any event, from a carrier perspective, the COLI business has not suffered at all, though at least some carriers are taking certain steps to guard against potential “antiselection” and other factors that may impact profitability if COVID surges again. Specifically, carriers are deemphasizing their corporate sponsored products (i.e., life insurance that employees choose to obtain with subsidies from the company) and focusing more on its corporate owned products (COLI, corporate owned annuities, and life insurance for groups of executives).

As I noted at the beginning, actuaries have a terrific record in evaluating and managing mortality risks, and Life Insurance companies continue to be some of the most solid and stable companies in the Financial Services sector of the economy. The clarity with which the industry has viewed the risks posed by COVID thus far gives me hope that the industry will continue to thrive.

However, the number of people who have died as a result of the disruption of our economy and healthcare delivery system that COVID has caused as well as the possibility of a resurgence of the disease in future years does suggest that actuaries and underwriters need to continue their vigilance regarding this risk if Life Insurance is to continue to play the critical role it has in providing financial security and stability to both individuals and corporations in the future.

If history is any guide, they will, and Life Insurance will continue to provide the financial security and stability to consumers and corporations alike that it has for over a hundred years.

I walk a lot these days – not because I need to, but because it keeps me close to the land

You see, a month ago I lost my land along with my home and everything in it.

It was the eve of Yom Kippur and when I woke that morning there was the familiar smell of smoke in the air. Living in rural Sonoma County I’ve become accustomed to the environment we now live in – Threats to health and welfare lurking all around us — unseen but still palpable and very real.

I checked the source of the smoke and found that the fire was just outside of Calistoga town of 5000 about 20 miles due east of me. That was concerningly close, but the wind was blowing south and in between it and me lay the town itself as well as miles of forest and Hood Mountain, a 2700-foot peak at whose base my 8.5-acre homestead lay, nestled against a spring fed creek that runs all year and up which salmon still swim.

Throughout the day I kept track of what was going on near Calistoga. Soon the fire had been named, and while that meant it had become a major problem, the news was still relatively encouraging in that Cal Fire was making this one a priority and was deploying an enormous number of resources to containing it and limiting its impact on the people who lived in Napa County where the fire was centered. I had been through this too many times before, including in 2017 when the Nuns Fire came within a mile of my property and so I was concerned but not overly so. I was confident that I and my neighbors would not have a problem with the fire itself though there was always the possibility that PG&E would shut off our power to prevent it from spreading. I was half-expecting that soon I would be getting a “prepare to evacuate” or even an “evacuation warning” text, but my phone is filled almost to capacity with those messages received over the last few weeks since fire season began, so while I don’t ignore them, I had, unfortunately, gotten too used to false alarms and was therefore wholly unprepared for what came next

Sometime in the middle of the afternoon, things took an ominous turn. A light dusting of ash started raining down on us and the quality of the air began to deteriorate badly. It took some time for us to figure out that the wind had shifted and that the fire was getting closer. This is when I made my next mistake. I assumed that since Calistoga was between me and the fire that if there was any danger, I would get plenty of warning because all those residents would need to evacuate first and that would give me plenty of time to get ready. It never occurred to me that the fire might simply go around the town and head straight for Hood Mountain.

Feeling worried, but in need of some grounding I attended my temple’s online Kol Nidre service – in some ways the most important holy day of the Jewish year. The service ended at 7:30 and by then the evacuation warnings were creeping closer.

I went to find my contractor Patrick, a brilliant and resourceful ex-football player from Georgia who was staying on my property while working on adding a bathroom and an outdoor kitchen to one of the out-buildings on my property. Having only been in Sonoma since June (he had come to visit my caretaker and find some work in the area), this was his first California fire season and even though I warned him that a wildfire was nothing to mess with, he seemed supremely calm and in control. I told him that the fire seemed to be headed our way and as he surveyed the property, he said that he thought that we would be ok, but he was going to start cleaning up the job site “just in case.”

Then things began to both speed up and to move in slow motion. A little after 8:30 an evacuation warning came through and I knew it was time to act. And here is where I made my final and most costly mistake. Instead of gathering stuff and packing, I spent the next precious 20 minutes walking through my house trying to decide what I would take if and when an actual evacuation order came. I asked Patrick if we had any boxes so I could start packing and he said that he thought there were some around, and while I started poking around, my mind fruitlessly started evaluating and prioritizing, mentally packing and trying to estimate what would fit into my pick-up truck and what I would have to leave behind because it was too bulky.

Then suddenly I was out of time.

At 9pm the evacuation order came, and now there was no mistaking what was happening. The fire was climbing up the back side of Hood Mountain and if it came down the other side we were in real trouble — right in the fire’s path backed up against a thick forest so tangled and overgrown that even walking through it on a normal day is a struggle. I couldn’t imagine how Cal Fire could possibly stop it if it ever got that far.

I was freaked, but at least I was now moving and acting. I had frittered away all my margin, and now could only grab and go. I got my passport, birth certificate, my will and a few other documents laying loose on my desk. I grabbed as many pictures as possible of my family I could throw into the one large suitcase I’d found and threw a few clothes into a gym bag that was lying on my bedroom floor. I made sure I got my laptops and some notebooks containing notes for my unfinished book manuscript, and on the way out I was able to pick up a couple of pieces of memorabilia like an album of my 1960’s baseball cards and a couple of Grateful Dead relics, but that was it.

I texted a friend in Berkeley to make sure I had a place to go and then asked Patrick to help me load the truck. At 9:15 I was driving down our private dirt road and eventually onto Los Alamos, then across 12 onto Melita Road taking the back way to 101 to avoid the rush. I got onto the highway just in time to get a frighteningly urgent follow up call from Sonoma County telling me to run for my life and as I headed south towards Berkeley, I passed a huge line of fire trucks coming up from Marin to fight the fire.

Meanwhile, despite my pleas that he also evacuates, Patrick stayed to try and save my house. Why he risked his life to save the home of someone he had only met a few weeks ago is still one of the great mysteries in my life but stay he did. For hours he fought desperately to save my house, hosing down the deck, digging fire breaks and moving equipment and lumber out of the way of the flames that were now on the land burning my stables and the redwood deck next to it. He worked side by side with the Cal Firefighters until after midnight when even he had to surrender to the overwhelming awesome power of nature’s fury. At the last minute he threw some tools into his little Mazda and drove through the flames right behind Cal Fire who themselves had just abandoned my home to fall back and fight the fire from Los Alamos a mile down the road.

It was only days later that I got the full story from Patrick. It seems that the fire came roaring down the mountain and then vacuumed through the little valley around the creek exploding into a firestorm that consumed everything along our dirt road only slowing down when it hit the pavement where Wildwood Trail becomes a public road. Patrick never had a chance, and yet some combination of courage, heroism and bull-headed stubbornness kept him fighting a hopeless battle against impossible odds until it was truly a question of living or dying. I am profoundly grateful he chose life, as otherwise I could never forgive myself for letting him stay and try to save my home.

Now three weeks later, I finally have a little space to call my own – a tiny studio apartment near downtown owned by Marta, the kind woman who runs a vintage clothes store in Railroad Square. She and others like her are what makes this community what it is and why I call it home. There is Linda who is an old Deadhead like me and still sells antiques out of a barn near town and there is her boyfriend Leo who lost everything he had in the fire as well but somehow still smiles and offers help to anyone who needs it. They had me over for a hot meal in her backyard the other night and even though they have each suffered grievous losses this year, they opened their house and their hearts to me. There is something uniquely wonderful about this town and the people who live here. Probably it comes from the fact that most of these folks have deep roots in Sonoma County and the catastrophes that keep visiting this place simply bring us all closer and make us more committed to look out for each other.

Wherever it comes from, Santa Rosa is a very special place and gives me hope for the future.

I walk a lot these days, not just because it keeps me close to the land, but also because it keeps me close to the people of this town and of this county. Even though COVID has made it dangerous to get too close, we are finding our way – to joy, to gratitude, to curiosity and to connection. Maybe we are even moving toward something a little lighter than the stormy darkness that surrounds us. Only time will tell.

I wanted my property to be a sanctuary – I’d even opened up a bank account to make it so. Valley Oak Sanctuary is the name I gave it in honor of the dozens of centuries old Oaks that lived on my land. Happily, many of them survived. My vision was for the property to become an island of peace and safety amidst the anger, conflict and danger that seems to surround us. That vision will now have to be deferred – at least for a while

And yet I know that Valley Oak Sanctuary will emerge once again, and while I don’t know when, how, or in what form it will take, I do know where it will be – at the end of a dirt road by a creek at the base of Hood Mountain. Hopefully it will happen soon, and while I can’t yet focus on rebuilding, when it happens, you will know. I won’t keep it a secret.

Keeping the lights on with home-cooked meals.

Keeping the lights on with home-cooked meals. About Peter Neuwirth: Since graduating from Harvard with a degree in mathematics and linguistics in 1979, Peter Neuwirth has held actuary leadership positions at consulting firms including Aon, Hewitt Associates, Watson Wyatt Towers, Perrin, and Towers Watson. He also ran the actuarial firm Coates Kenney and spent a year at Price Waterhouse.

About Peter Neuwirth: Since graduating from Harvard with a degree in mathematics and linguistics in 1979, Peter Neuwirth has held actuary leadership positions at consulting firms including Aon, Hewitt Associates, Watson Wyatt Towers, Perrin, and Towers Watson. He also ran the actuarial firm Coates Kenney and spent a year at Price Waterhouse.

Rita asks Peter:

Rita asks Peter: